By Jock Finlayson, ICBA Chief Economist

Health care stories have become a staple of the daily news, with millions of Canadians struggling to find a doctor, hospital emergency rooms frequently overwhelmed, and the country’s once vaunted “public” health care services appearing to crumble. If there is a root cause of what increasingly looks to be a failing “system,” one is hard-pressed to conclude that it’s a lack of money. Canada currently devotes 11.2% of its GDP to health care. Among advanced economy jurisdictions, only the U.S., Germany, France, and Sweden allocate larger fractions of GDP to provide health services.

According to the Canadian Institute for Health Information’s (CIHI) latest review, overall health spending is on track to reach $400 billion this year, up 4.2% from 2024. Measured in current dollars, health care outlays have approximately doubled since 2010.

The public sector – the federal, provincial and aboriginal governments combined – accounts for 71 cents of every dollar spent on health care, with the private sector picking up the rest. Private sector spending goes for services not covered by provincial Medicare plans (e.g., cosmetic treatments, vision care, and most dental services), services that are fully or partly paid through employee health and dental plans (like those administered by ICBA), and some other categories. Of interest, among developed countries Canada is second only to the United States in the proportion of total health care spending that falls on the broadly defined “private sector.”

By component, hospitals make up 26% of Canadian health care spending, with half of this earmarked to pay the salaries, wages and benefits of hospital-based employees. Physician services account for 14%, followed by drugs at a little over 13%. Drug costs are climbing as new treatments and therapies come to market – such as high-cost biologics, weight loss drugs, and specialty drugs that target genetic disorders. The other main health spending categories are home and community care, seniors’ long-term care homes, and non-medical professional services (e.g., dentists and physiotherapists). It should be noted that less than 5% of all health spending in Canada goes to finance capital projects and technology upgrades. This helps to explain the dilapidated state of many hospitals and other health care facilities and the sector’s out-of-date IT infrastructure.

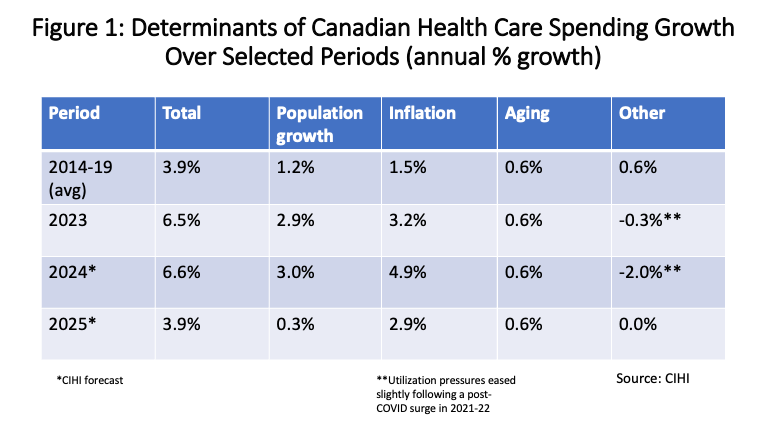

As the CIHI’s report summarizes, “Canada’s health care spending is driven by supply and demand factors including inflation, population growth, population aging and service utilization.” The various determinants of health care spending growth since 2014 are broken out in the first accompanying figure. Inflation pressures have played an outsized role in recent years. Population aging is an ongoing but slow-moving trend. No data are provided for the years 2020-2022 because of temporary disruptions and distortions caused by the COVID-19 pandemic. Utilization of health services fell in the early stages of the pandemic but then surged in the second half of 2021 through 2022 before dipping slightly in 2023-24.

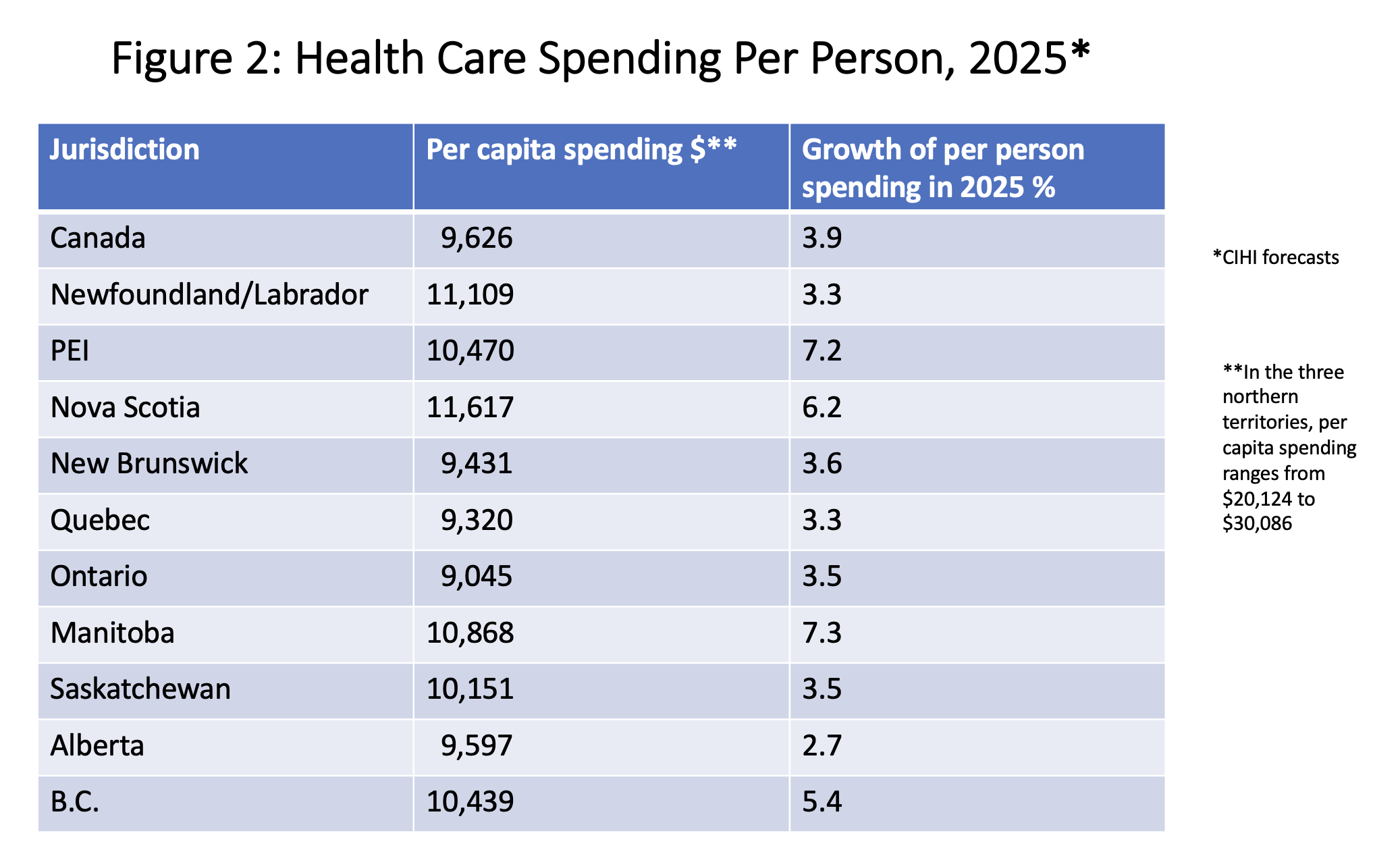

There is some variation across the country in the growth of health care spending over time as well as in the distribution of spending by component. Figure 2 show health expenditures per person and the growth of such spending in 2025, based on CIHI’s most recent forecast. The northern territories are far and away the biggest per capita spenders, owing to their small and widely dispersed populations and challenging geographic and climatic characteristics. Among the ten provinces, Newfoundland and Nova Scotia spend the most per person while Ontario spends the least. B.C. spends more on health care than neighbouring Alberta, likely a reflection of its older population. In 2023, people aged 65 and over accounted for almost half of all health care spending in Canada, while making up just 19% of the country’s population.

Looking ahead, CIHI expects aggregate health care spending to outpace GDP growth. However, with governments under mounting fiscal pressure, it is likely that the private sector – employers, insurers and households – will end up shouldering a bigger portion of health-related costs, notwithstanding the federal government’s recent moves to expand the public sector’s role in covering some drug and dental costs.