By Jock Finlayson, ICBA Chief Economist

Amid the daily deluge of economic news – much of it focused on topics such as job growth, housing markets, the impact of innovative technologies, and government budgets – it is easy to lose sight of a basic but important fact: the economy is made up of distinct industries. Most of these industries, in turn, are populated by profit-seeking business enterprises which, collectively, underpin and drive the bulk of all economic activity.

In both the U.S. and Canada, statisticians categorize industries based on the North American Industry Classification System (NAICS). The NAICS divides the economy into hundreds of narrowly-defined, specific industries. For economists, it is common to group these into 19 or 20 aggregate categories, each of which contains multiple individual industries. Construction is one example of an aggregate industry category under the NAICS, along with manufacturing, health care, retail trade, etc.

We can use the NAICS analytical framework to help us understand the structure and evolution of the economy over time. This post looks at Alberta’s industrial structure through the NAICS lens.

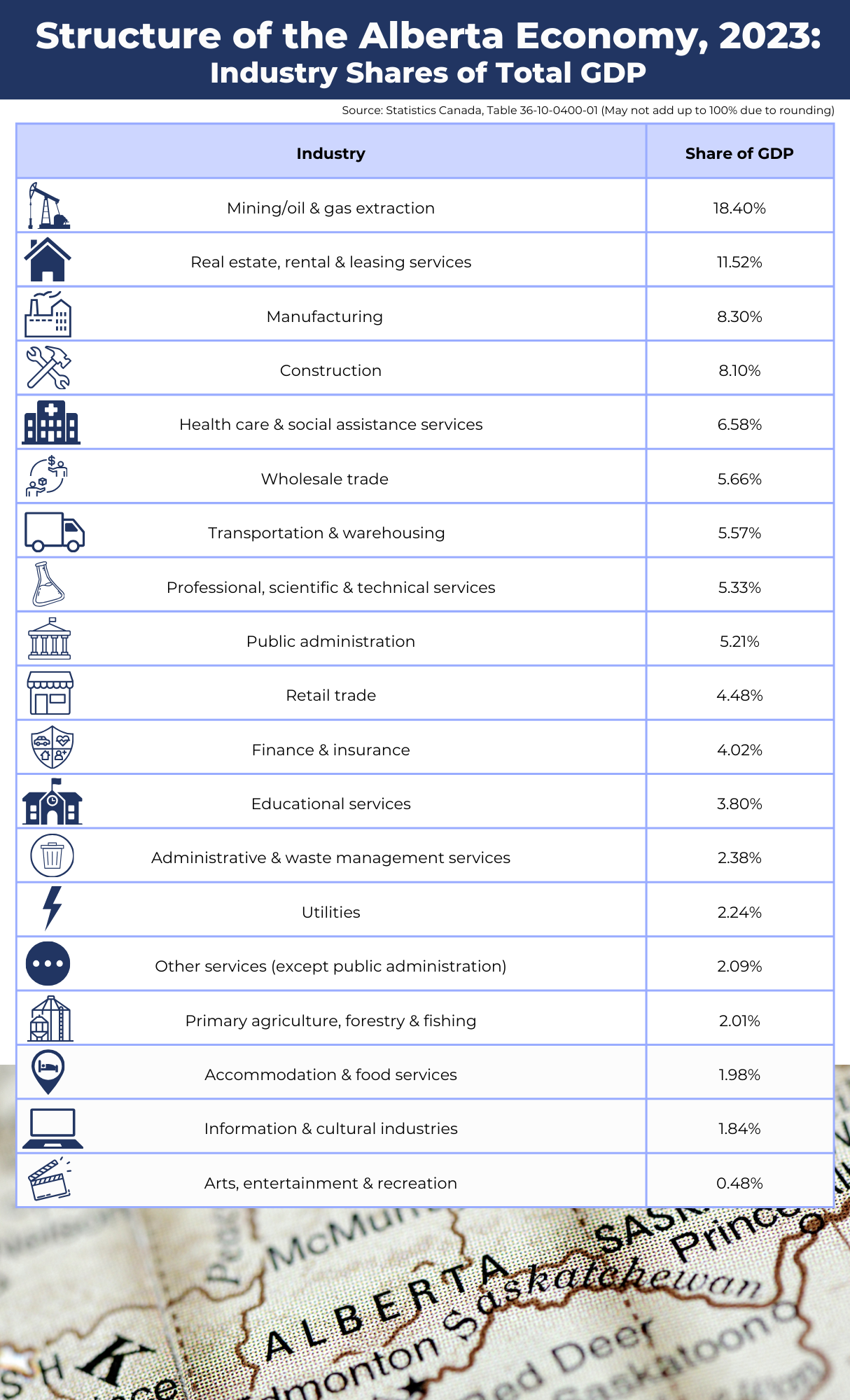

The accompanying table shows the percentage shares of Alberta’s economic output (gross domestic product at 2017 prices) accounted for by the principal NAICS-defined sectors as of 2023. Here, the economic output of a given industry means the “value-added” attributable to that industry. “Value-added” is measured as the difference between 1) the selling prices of the goods or services produced by an industry, and 2) the cost of the “inputs” used by that industry to produce those goods or services. Because public sector industries generally don’t operate with market-determined “selling prices,” a different approach is used to estimate their “value-added” contribution to economy-wide output.

The accompanying table shows the percentage shares of Alberta’s economic output (gross domestic product at 2017 prices) accounted for by the principal NAICS-defined sectors as of 2023. Here, the economic output of a given industry means the “value-added” attributable to that industry. “Value-added” is measured as the difference between 1) the selling prices of the goods or services produced by an industry, and 2) the cost of the “inputs” used by that industry to produce those goods or services. Because public sector industries generally don’t operate with market-determined “selling prices,” a different approach is used to estimate their “value-added” contribution to economy-wide output.

A few interesting points emerge from the data presented in the table.

One is the wide variation in the “size” of the 19 aggregate NAICS categories, ranging in Alberta’s case from more than 18% of GDP for the biggest sector (mining and oil/gas extraction) to less than 0.5% for the smallest (arts, entertainment, and recreation).

Second, Alberta’s economy has become increasingly services-oriented, with service-producing industries now comprising more than three fifths of GDP, up from 55% two decades ago. Goods producing industries – including construction – are responsible for the rest. Because of the outsized role of the energy sector in Alberta, goods-producing industries occupy a larger place in its economy than is the case elsewhere in Canada.

A final point: despite what some people may believe, Alberta remains overwhelmingly a “market economy,” in the sense that the vast majority of GDP is generated by and in the private sector. Together, the three main “public sector” industries – public administration (capturing all levels of government), education, and health care – represent less than 16% of GDP, and a portion of this actually captures private sector production (e.g., private education; dental and physiotherapy services). This means that substantially more than four-fifths of all economic output in Alberta comes from the broadly defined business sector.

A few key industries…

Mining and oil and gas extraction ranks as Alberta’s number one industrial sector (18.4% of GDP) under the NAICS framework. This is not surprising, given that the energy sector (driven by upstream oil and gas) supplies most of the province’s exports and boasts very high levels of productivity (GDP per hour) compared to other industries. Even so, mining and oil and gas extraction is less dominant today than it was in the early 2000s, when it made up more than one-quarter of Alberta’s GDP.

Real estate, rental and leasing services (11.5% of GDP) is the second biggest NAICS industry cluster. It consists of businesses engaged in renting, managing, leasing or otherwise allowing the use of property, buildings and other tangible assets (like vehicles and equipment), as well as businesses which act as intermediaries in the sale/rental of real estate or provide services such as appraisal. It does not include business involved in the construction of buildings or land assembly/development.

Manufacturing’s share of Alberta’s GDP has been relatively stable since the early 2000s, in contract to the pattern in other provinces where the sector has dwindled in size. Manufacturing produced 8.3% of Alberta’s economic output in 2023. Within the manufacturing category are dozens of individual industries, including several — like petrochemicals, lumber, pulp and paper, and food manufacturing — that are focused on the further processing of Alberta-origin primary resources.

Construction emerges as Alberta’s fourth largest industry, directly responsible for a little over 8% of total output. Under NAICS, construction has three principal sub-sectors – building construction, heavy civil and engineering construction, and speciality trades contractors – which at a more granular level are divided into 29 individual construction-related industries.

Among the broad NAICS industry sectors dominated by government, health care and social services is the biggest (6.6% of GDP in 2023).

Other aggregate NAICS sectors that produce at least 5% of Alberta’s economic output are transportation and warehousing; professional, scientific and technical services; wholesale trade; and public administration.

Understanding the structure of the economy is a vital task for business analysts and policymakers alike. One often sees elected officials breathlessly lauding the purported growth potential of very small industries – “clean tech” being a recent example. As a matter of basic arithmetic, even if tiny industries grow rapidly, their small size will limit the quantum of “extra GDP” that results. At the same time, there is a tendency among some policymakers and media commentators to ignore or discount the economic contributions of large industry sectors like oil and gas, construction, manufacturing, and wholesale trade. Over time, this kind of blinkered vision can undermine the growth potential of the entire economy.